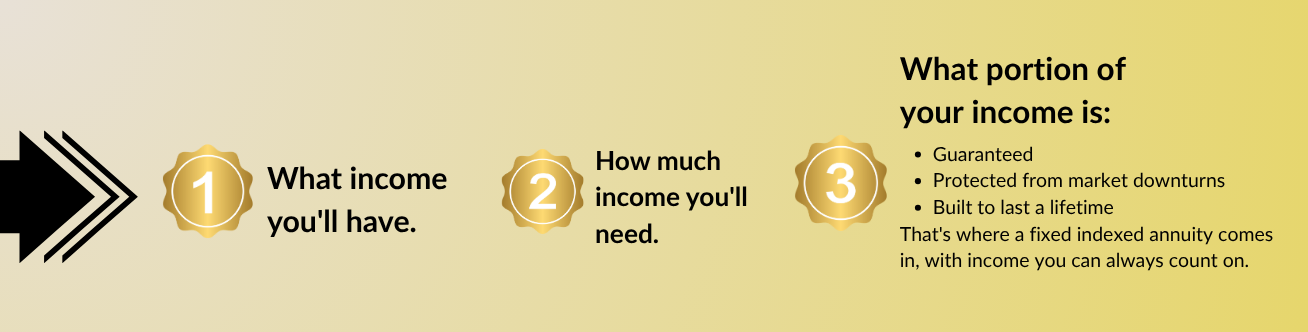

If you have 5-15 years before retirement, now can be a good time to make sure you’re on track and to start thinking about how to turn your savings into future retirement income. Talk to your financial representative about:

A fixed indexed annuity (FIA) with a Guaranteed Minimum Withdrawal Benefit (GMWB) gives you a predictable way to build your future retirement Income base for a steady stream of lifetime income — without the risk of actually participating in the market.

When it comes to your hard-earned retirement savings, does the thought of letting your money ride with the ups and downs of the stock market give you an uneasy feeling? But you don’t want to miss out on the sharing in some of the potential gains? A more conservative solution, called a fixed indexed annuity (FIA) may be right for you.

An FIA gives you protection from market losses and growth potential based on a market index (like the S&P 500®) — without the risk of actually participating in the market.

Many annuities allow for penalty-free withdrawals and amounts in excess of the penalty-free amount may be subject to surrender charges. Many F&G annuities include riders, at no additional charge, that give you penalty-free access to 100% of your money if you meet certain conditions in regards to terminal illness or nursing home or home health care. These liquidity features may vary by state. Talk with your independent producer for availability.

Fixed and fixed indexed annuities that haven’t been annuitized have surrender charges waived if the annuitant dies. Any remaining account value is passed to the beneficiaries you named and usually avoids probate.

You are not required to pay the insurance agent directly in order to buy an annuity. Your full premium is available to potentially earn interest from the annuity’s effective date. F&G products are only offered through our licensed insurance producers, who are compensated through commissions which are not deducted from the premium paid for the policy.

Depending on the type of annuity you purchase (immediate, fixed or fixed indexed), your policy could have no charges. But some annuities do have surrender charges on withdrawals taken during your surrender charge period. Some plans may offer options to take a portion surrender-penalty free. Plus, some fixed indexed annuities have additional fees with optional riders for guaranteed lifetime income, a specific growth rate, wealth transfer and healthcare. These features provide more benefits and can add more value to your policy.

Annuities with a guaranteed lifetime withdraw benefit work similar to Social Security or a pension. It can guarantee you a lifetime stream of income, subject to certain conditions and assuming no excess withdrawals are taken.

With a fixed indexed annuity, your money is not invested in the market, but it provides the potential to earn interest linked to an index. So your account value will never be credited less than zero if the index decreases. Plus your account value can grow if the index increases.

We’ll help you take the next step in planning your financial future.

For inquiries regarding our professional consultancy and insurance services, feel free to contact us through the provided channels – we’re here to assist you seamlessly.