Registered Index-Linked Annuities (RILAs) are designed to offer greater potential for interest growth, making them an attractive option for those who seek more growth potential than fixed or fixed-indexed annuities, and are willing to accept additional risk.

Is finding the right balance between protecting your principal and pursuing growth top of mind? If so, RILAs can be an integral part of a long-term retirement strategy.

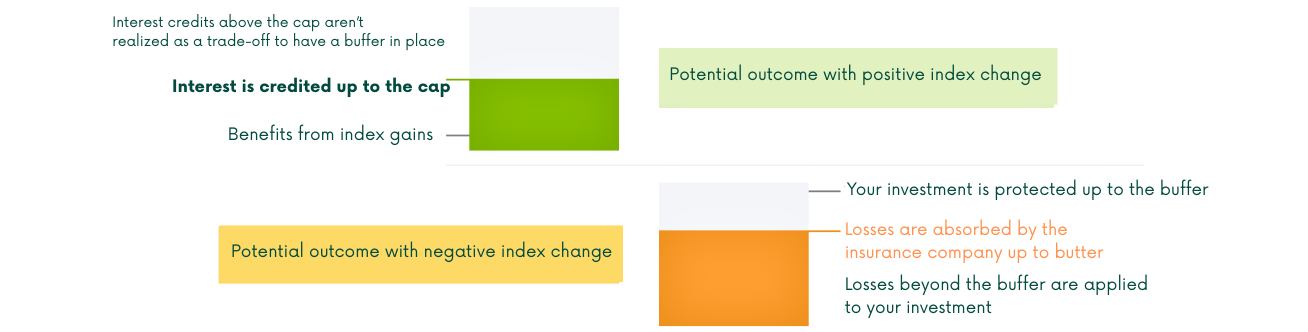

RILAs utilize the performance of an external market index to determine potential gains and losses. While RILAs may have limits on the upside in the form of caps, you are also shielded from complete exposure to market downturns, thanks to a level of downside risk in the form of buffers.

Each index-linked interest crediting strategy has a crediting method, crediting period and is tied to a market index. Interest to be credited (which may be positive, negative, or equal to zero) is determined at the end of the crediting period. Prior to the end of a crediting period, an interim value will apply to the account value. That means the account value will be adjusted based on market factors and the adjustment can be positive, negative or equal to zero. Before investing in a RILA, talk with your trusted financial professional to ensure you understand the complexities specific to that product.

The selections you make in a RILA can help you strike a balance between risk and potential reward.

When the index return is positive, you participate in a portion of potential market index gains and earn interest on your premium.

When the index return is negative, your premium is protected up to a stated percentage, called a buffer. Then you are responsible for any losses beyond the buffer. Loss of principal is possible. It is important to talk with your trusted financial professional to ensure you understand the risks associated and make informed investment decisions.

Buffer: The buffer is the percentage of negative index change that can occur before you are credited with negative interest credit. In other words, a buffer protects you from a percentage of loss. You take on any percentage of loss that is in excess of the buffer percentage.

Cap: A cap is the maximum interest rate you can earn, regardless of the change in the index. Interest rate caps designate the ceiling, or maximum gains, for indexed annuities.

Crediting method:How the interest credited is determined.

Crediting period: The investment period over which the index performance is measured to determine the interest credited.

Index-linked crediting: Index-linked crediting uses the performance of an index to determine how much interest is credited to the annuity value.

We’ll help you take the next step in planning your financial future.

For inquiries regarding our professional consultancy and insurance services, feel free to contact us through the provided channels – we’re here to assist you seamlessly.